ESOPs are projected to be the biggest transfer of wealth in U.S. history.

A discussion regarding Employee Stock Ownership Plans (ESOPs) must contain the obligatory ESOP basics, including an ESOP definition, as well as the advantages to the seller, company and employees. This article will briefly do the same, but will focus mainly on the non-leveraged ESOP, the simplest of all ESOP designs, and also why they are making a significant resurgence due to the current economic environment.

ESOPs Now More Than Ever

In light of the current and projected economic and tax environment, ESOPs are gaining momentum as baby boomers look to transfer their businesses in a way that is most favorable based on their families’ goals and objectives. It is projected to be the biggest transfer of wealth in U.S. history, estimated at $15 trillion or more over the next 15 years. A substantial portion of these baby-boomer owned businesses are family businesses that would like to perpetuate the business into the next generation or key management, but do not wish to give the business away. The next generation often cannot afford or even borrow the purchase price.

The owner also faces considerable taxation on stock sale proceeds including capital gains tax due to a potentially very low or zero cost basis and considerable corporate and personal income taxation. According to current tax law taking effect January 1, 2013, the tax burden on a selling shareholder only gets more onerous. Federal capital gains rates increase to 20% from 15% plus any applicable state capital gains tax, as well as rising income tax rates. Additionally, the recently passed health care legislation imposes a 3.8% tax on the gain portion of a business sale effectively making the federal capital gains rate 23.8% plus any applicable state capital gains tax.

ESOPs have unique procedural and tax benefits that are NOT affected by the tax law changes effective January 1, 2013. ESOPs may not be subject to the underlying affected capital gains or income taxes at all. A non-leveraged ESOP also has the potential to avoid the temporary suppression of the business value due to economic conditions and allow the owner to enjoy the full “true value.” Therefore, ESOPs are one of the best and most tax efficient ways for a business owner to transfer a business to the next generation and the reason for the resurgence of the non-leveraged ESOP.

Employee Stock Ownership Plans

Technically, an Employee Stock Ownership Plan, or ESOP, is a defined contribution, government sanctioned tax-qualified retirement benefit plan under Internal Revenue Codes 401(a) and 4975(e)(7). An ESOP is mandated to “invest primarily in employer stock” and is overseen by both the Internal Revenue Service and the U.S. Department of Labor.

In more practical terms, an ESOP is a highly tax advantaged, immediate or gradual exit strategy for business owners. The ESOP is a “ready and willing” buyer of the seller’s stock that keeps out unrelated third parties and allows corporate control to be unchanged. It retains the seller’s existing perks while providing significantly enhanced retirement benefits to all eligible employees who will have a beneficial ownership interest in the stock sold to the ESOP.

ESOP Advantages

The advantages of an ESOP are many and varied, covering both financial and “piece of mind” issues for the seller, company, employees and community.

The seller enjoys an immediate buyer of some or all of the seller’s stock at fair market value as outlined by Revenue Ruling 59-60 and may indefinitely defer all capital gains tax on sale proceeds under IRC§1042. The seller can retain personal salary, benefits and corporate control that can be transferred according to the seller’s timetable.

The company may perpetuate in an orderly manner without a dramatic change in control and without the interference of outside buyers who may have conflicting corporate objectives. The company sponsoring an ESOP receives a dollar for dollar corporate income tax deduction on the entire stock purchase price, within limits, and statistically outperforms its non-ESOP peers through improved employee motivation, morale and “skin-in-the-game.”

Employees and their family benefit from an ESOP by significantly enhanced retirement benefits with no out of pocket costs. The employees share in the value of the company in which they helped build and grow through beneficial stock ownership. Additionally, the orderly internal transfer of the company, compared to an outside third party sale, creates a more stable and reliable community employer.

ESOP Structure

Usually an ESOP structure discussion begins with the non-leveraged ESOP followed by the usual focus of the leveraged ESOP and its many advantages; however, this discussion will begin with the leveraged ESOP then proceed to the main point of this discussion, which is the non-leveraged ESOP.

Leveraged ESOP An ESOP, unlike any other qualified retirement plan, is allowed to borrow, or leverage, the funds required to buy the desired shares from the selling shareholder. The company usually makes annual tax-deductible contributions to the ESOP, which uses the contributions to repay the loan incurred to buy the stock until the debt is repaid. In other words, the entire principal and interest on the loan incurred to buy the seller’s stock is completely income tax deductible to the company within limits and the sale proceeds are potentially 100% capital gains tax-free to the seller. This structure involves an immediate stock sale at current fair market value.

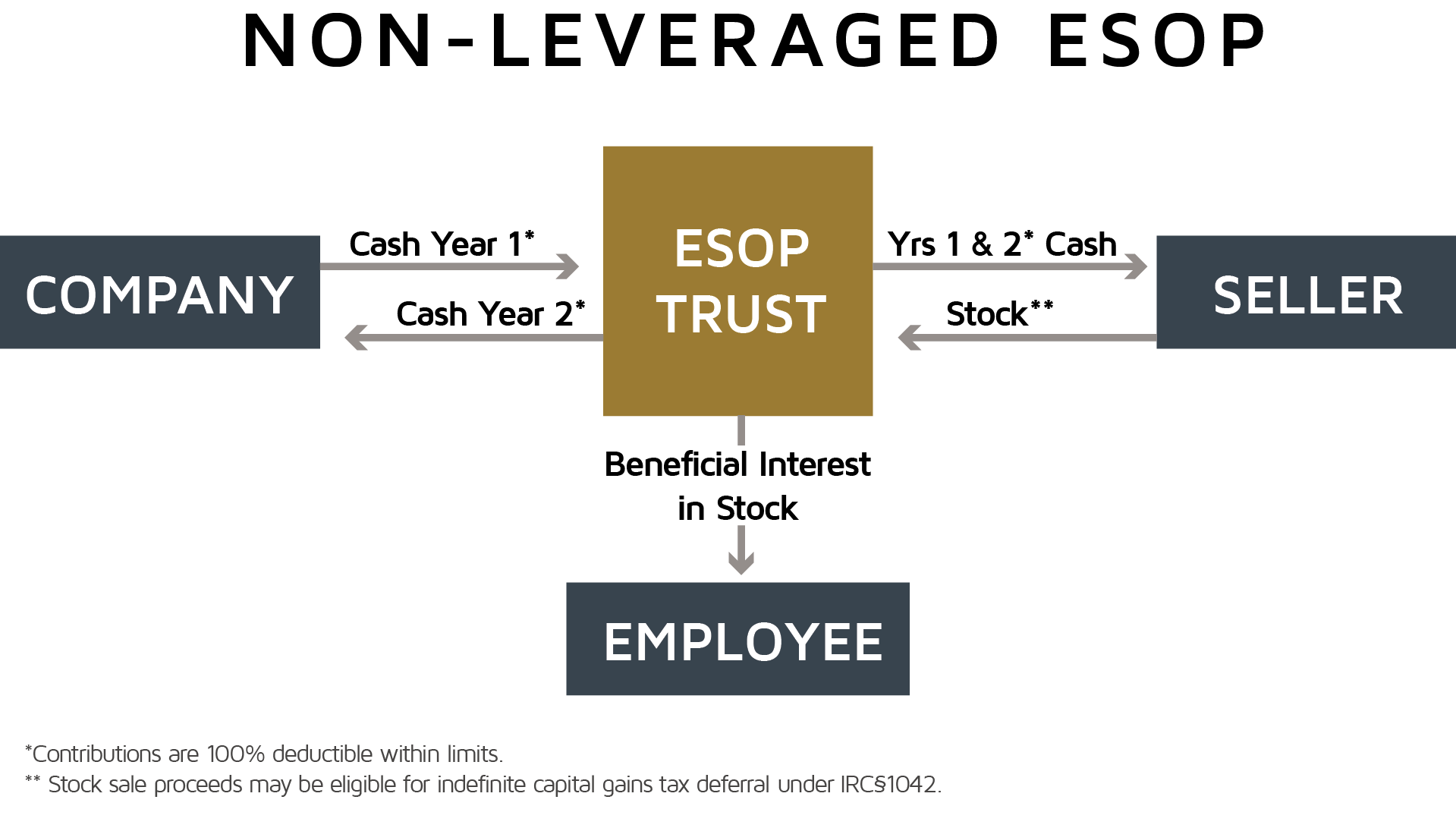

Non-leveraged ESOP A non-leveraged ESOP does not borrow the funds to buy shares from the seller. Instead, the sponsoring company contributes newly issued stock, existing treasury stock or cash to the ESOP, which is used to buy shares from the selling shareholder. If shares or cash are contributed to the ESOP, the company receives a current income tax deduction for the amount of the contribution subject to certain limits. If the company contributes cash to the ESOP, the ESOP may maintain a cash account for up to 2 or more years before it is required to fulfill its mandated mission, to “invest primarily in employer stock” which means it must buy stock from seller or convert to a non-ESOP plan.

Current Economic Conditions and Effect on Business Value

Many business owners are currently experiencing a revenue decline based on the economic environment, not necessarily a flaw in business practices or strategy. In fact, many companies experiencing a decrease in revenue and profits are faring quite well in relation to their peers. For business owners considering selling some or all of their stock, the economic downturn has a negative impact on both the seller’s stock value and the number of willing and financially able buyers. A buyer’s offer is determined by many factors and by several methods. Regardless of primary valuation method employed, the buyer or valuator will factor in the trailing twelve months (TTM) of revenue, which may not reflect the company owner’s perceived “true value.” Additionally, the common discounted cash flow (DCF) method bases the stock value on the projected cash flows of the company. These projections may not be back to “normal” in the near-term even in an immediate business and economic upturn therefore contributing to the depression of the true value of the business.

The Dilemma

Business owners face a dilemma concerning their business exit and transfer options. On one hand, they would like to begin the process of an orderly, systematic sale and transfer of the business to the next generation, key management or buyer as soon as possible. On the other hand, business owners are not happy with the current value of the business based on economic conditions and would prefer to wait sell to sell stock until the business value rebounds closer to the owners’ perceived true value.

The Non-leveraged ESOP Solution

The non-leveraged ESOP may be the ideal solution to the business owner’s dilemma. A non-leveraged ESOP offers the best of both worlds: It allows the owners to begin the tax advantaged transfer process now, but actually sell the stock at a later date when the market value may be closer to the owner’s perceived true value.

Here is how the basic non-leveraged ESOP would accomplish these two goals and solve the dilemma. As discussed earlier, an ESOP is a government sanctioned tax qualified retirement plan designed to primarily invest in employer stock, however, it is not required to immediately do so. Generally, the ESOP has two or more years to maintain a cash position before it is required to fulfill its statutory objective of investing in employer securities. Many business owners are very confident that the fair market value of the business will be closer to their perceived true value in two years from the implementation of the ESOP. If not, they very often feel that the value will not substantially decline more than it already has. Therefore, a stock sale in two years can allow the owner to benefit from a substantially higher sale price than a current stock sale would yield.

The question then arises “Why not just wait two years to install the ESOP instead of implementing it now?” The answer is that by currently installing the tax qualified ESOP; the company can mitigate current income taxation by fully deducting current contributions to the ESOP, within limits, that will eventually be used to purchase stock from the owner. In other words, the owner is building a tax-deductible cash reserve in the ESOP until the seller is comfortable with the stock price and is ready to sell stock to the ESOP. The non-leveraged ESOP is a very flexible ESOP model since the company is making contributions to the ESOP at the owner’s discretion, not based on a rigid loan repayment schedule like a traditional leveraged ESOP. Many times ESOP contributions are simply a redirection of contributions previously budgeted for other corporate retirement plans.

Future flexibility

In two or so years the owner has several options. First, at the seller’s discretion, the ESOP can use its cash reserve plus any current-year contributions to purchase a block of stock from the seller. The seller may still enjoy the potential indefinite deferral of the capital gains tax afforded to sales of stock to an ESOP upon meeting the standard requirements. In fact, the ESOP may need time to build the reserve over several years to have enough cash to purchase the minimum 30% of outstanding company stock required to defer the capital gains tax under IRC§1042.

The second option is to use the cash reserve and any current year contribution plus the addition of a bank or seller financed loan (leveraging) to purchase stock from the seller. By converting the non-leveraged ESOP to a leveraged ESOP, the seller may potentially sell a larger block of stock than relying on annual contributions alone. However, the annual contributions to the ESOP become more inflexible due to the ESOP’s loan repayment obligations.

Lastly, should the owner decide to not sell to the ESOP after two or more years for any reason, the previous contributions in the plan simply get converted to another non-ESOP employee retirement plan. The owner’s reasons not to sell to the ESOP could include continued dissatisfaction with the value, a decision to sell to an outside buyer or other reasons.

Conclusion

It is clear that the resurgence of the non-leveraged ESOP is not surprising in an economic environment where a growing number of baby boomer business owners are looking to begin an orderly, tax-efficient transition of control and ownership to the next generation, but face the reality of a currently suppressed business value. A non-leveraged ESOP can be the solution offering the best of both worlds by beginning the transition process, yet capturing the owner’s perceived true value due to the unique attributes afforded to only ESOPs by the U.S. tax code. When evaluating an owner’s transition options, the piece of mind uniquely afforded to a non-leveraged ESOP is unparalleled when it comes to after-tax sale proceeds to the seller, corporate and personal tax advantages, future decision choices and contribution flexibility. It has never gone away, but may have been forgotten until the economic conditions and tax environment have proven to be just right for the resurgence of the non-leveraged ESOP.